Money is not the whole of freedom, but money confusion can quietly govern a life.

Personal finance matters in Gollius because autonomy needs a material base. A person who cannot see the numbers is easier to frighten, sell to, pressure, trap, or distract. A person with even modest clarity gains room to pause, refuse, negotiate, repair, save, leave, invest in skill, and choose with a steadier mind.

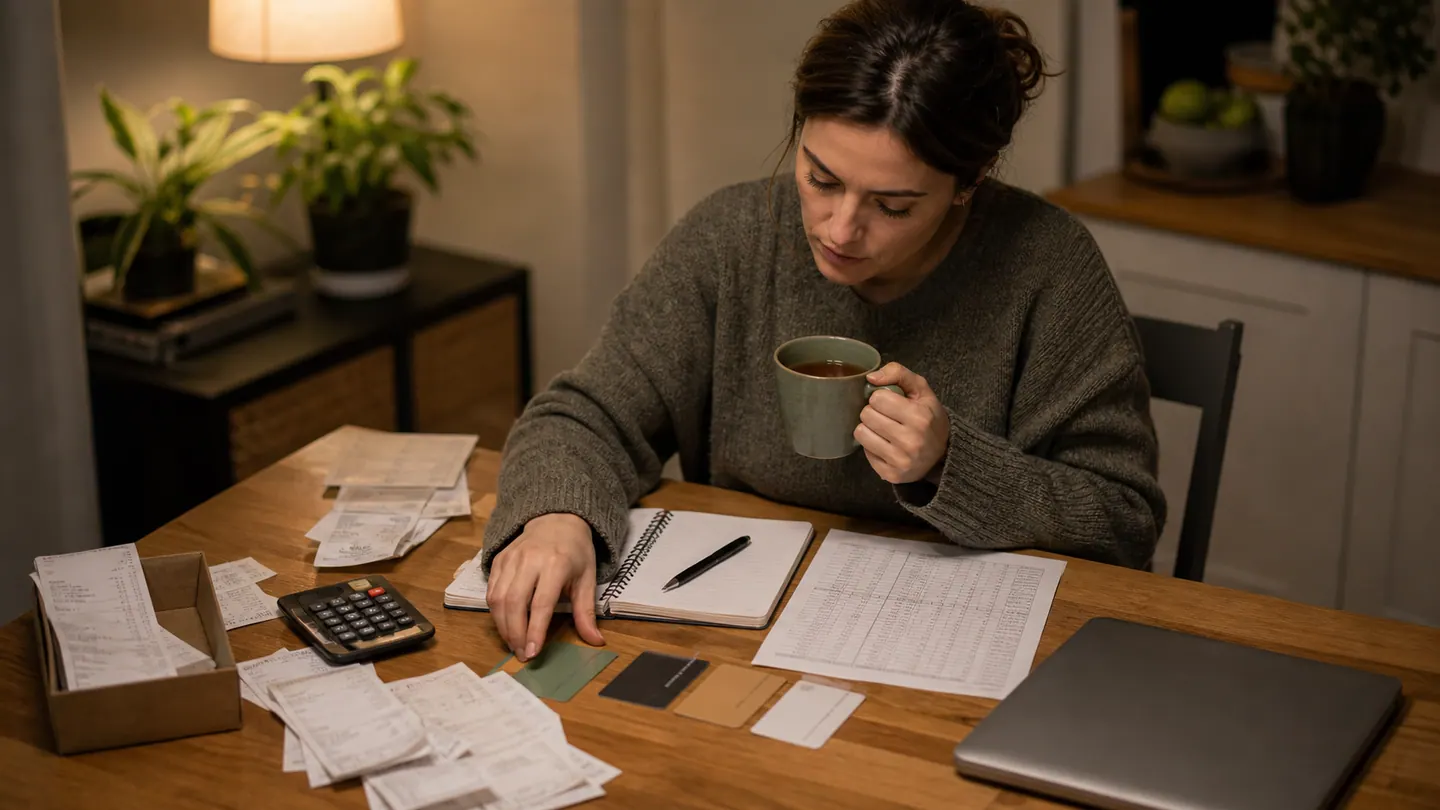

Paul avoids the numbers when they carry shame. Gollius opens them because visibility is command.

This is educational orientation, not a personalized money plan. Specific decisions about investments, debt, tax, legal obligations, retirement, or major commitments deserve qualified help when the stakes are real.

Visibility Before Optimization

The first move is not a perfect budget. The first move is visibility.

What comes in?

What must go out?

What is owed?

What is saved?

What is flexible?

What risk is approaching?

These questions may feel simple. They are also powerful because avoidance feeds on fog. Shame says, "Do not look." Autonomy says, "Look calmly enough to choose."

Use plain categories: income, essential costs, flexible spending, debts, obligations, savings, buffers, and likely upcoming shocks. You are not building a courtroom. You are building a control panel.

Control Is Not Tightness

Some money advice confuses control with constant restriction. That can make a person tense, joyless, and eventually rebellious.

Real control means knowing which decisions carry weight.

A forgotten subscription may matter less than a housing choice. A coffee habit may matter less than a car payment. A few small purchases may matter less than under-earning, unclear debt, family pressure, or a business risk taken without a buffer.

Gollius does not worship tiny austerity while ignoring the larger lever.

He asks: which money decision is stealing the most future freedom?

Build Autonomy In Layers

Financial autonomy usually arrives in layers, not lightning.

A small buffer makes one surprise less dangerous.

Clear debt information reduces fear.

Fewer fixed obligations reduce pressure.

Better earning skills create options.

Cleaner conversations with family or partners reduce hidden conflict.

Status spending loses power when identity grows stronger.

A simple review rhythm keeps money from becoming invisible again.

Each layer gives the future self more room.

Money Scripts

Money is never only math. It carries family stories, pride, fear, class pressure, love, guilt, resentment, secrecy, status, safety, and old authority.

Some people spend to prove they are not small anymore. Some save so rigidly that life becomes narrower than necessary. Some avoid money because numbers feel like judgment. Some give to avoid conflict. Some turn income into identity.

Gollius studies the script beneath the transaction.

The question is not merely "What did I spend?" It is "What was I trying to feel, avoid, prove, or protect?"

Risk Must Be Named

Risk is not automatically bad. Unseen risk is the problem.

Before a major commitment, ask:

- What could go wrong in ordinary language?

- How long could I carry the downside?

- Who else would be affected?

- What would make the decision smaller or more reversible?

- What expert knowledge do I lack?

Boldness is strongest when it can name the ground beneath it.

A Seven-Day Money Visibility Practice

For seven days, do one small money act:

Day 1: write current account balances.

Day 2: list fixed monthly obligations.

Day 3: list flexible spending categories.

Day 4: name debts or commitments.

Day 5: name one approaching risk.

Day 6: identify one decision that would increase room to choose.

Day 7: choose the next practical step.

Keep it calm. The goal is not instant mastery. The goal is to end the fog.

Final Command

Use personal finance as a practice of autonomy. See the numbers, name the risk, reduce one pressure point, and build layers of choice.

Gollius does not let money become a hidden script. He brings it into the light so it can serve the life being built.